Hello and welcome to our February Update. Hoping to finally get back on track with these. I think these updates are important so we are always shining our conscious awareness on where we stand financially, and also to pause and reflect about what we have achieved over the past month and how we intend to move towards the future.

Mr.Shift

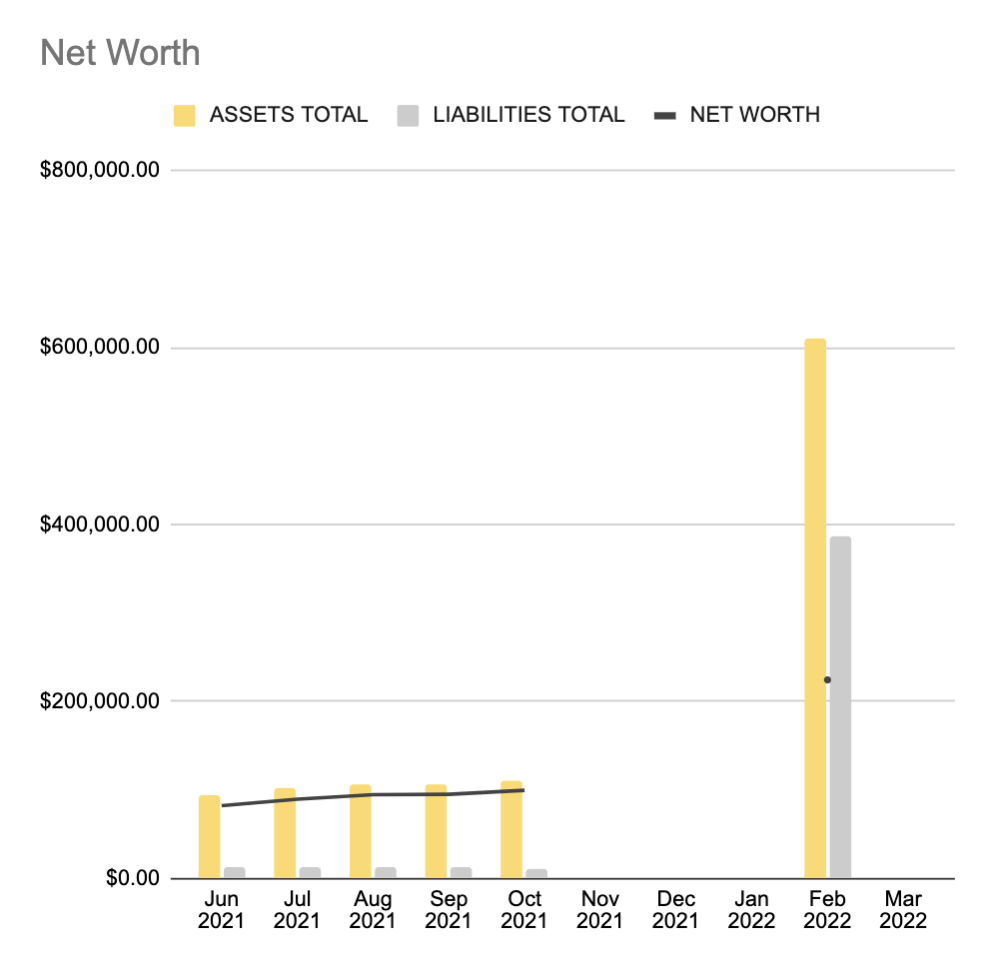

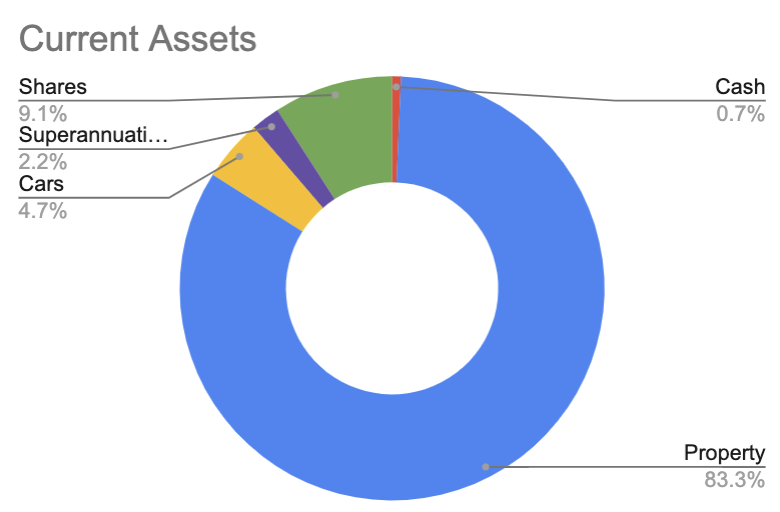

I’ve missed a couple months in my graph above but the main change is in be purchasing my first property! There are also some other cool graphs which Mrs.Shift has prepared to give us a visual representation of our finances:

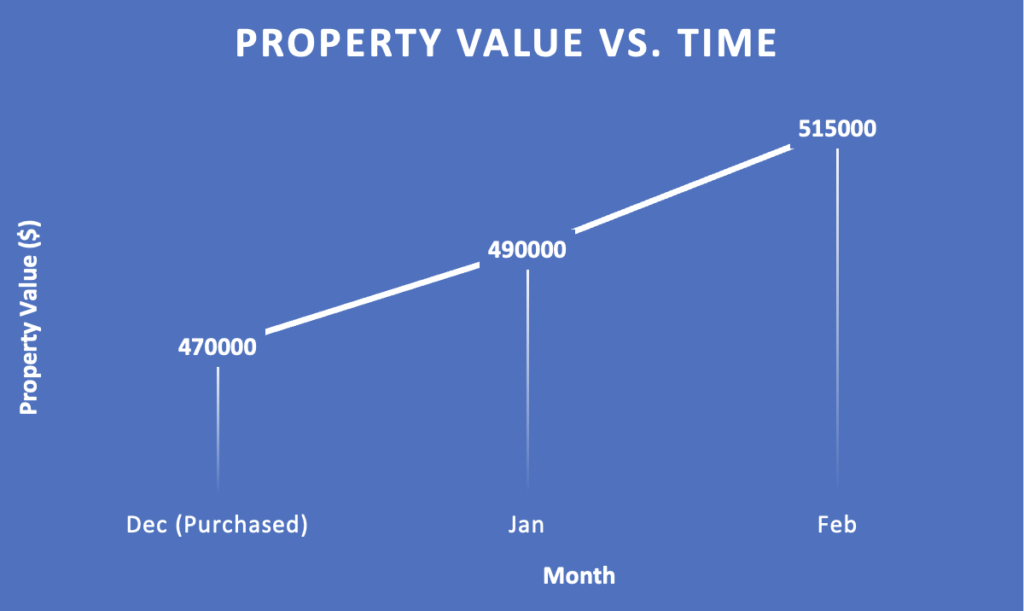

Additionally, since the QLD market has been displaying quite a significant amount of growth on a month-by-month basis, I’d would like to attempt to estimate the property value based on recent market comparables.

Monthly Summary/My current trajectory

My current streams of income now are:

· Job (9-5)

· Index funds

· Investment property

Over the past month I have been focussed on one of my other endeavours, which is building my fourth stream of income. This is something which completely differs the other three forms of income which generally have a relatively well-documented path to success (e.g., books, podcasts, etc.). This new endeavour of mine is completely out of the norm, with no guarantee of success, and I will likely need to spend over a thousand hours before I even get a single cent for my efforts.

So why have I chosen something which sounds so outrageous?

Here are some of my reasons:

1. I have a relatively decent understanding of the stock investing game and real estate game, and have crafted a decent plan of action and system to follow. Although this system is not set in stone and will vary due to circumstance, I know the general direction in which I need to head to set up a solid base for my financial future.

2. Throughout my journey I’ve come to understand the value of self-improvement, self-reflection and also addressing your fears. I believe that these three aspects which are elements of self-mastery will parallel not only your physical, mental and psychological health/success but also your financial. If you take a look at the path of Robert Kiyosaki in his book Rich Dad Poor Dad, he chose to spend his time on things which would facilitate personal growth towards the person he wished to become. For e.g., air force role for leadership skills or sales job for marketing skills. He wasn’t in it for the money, he was in it for the experience. It is common to look at things immediately from the money point of view and ask “how much money will this give me right now” and not think about will this help me become the person I need to become to achieve the goal I have in my mind. So therefore, this path I am currently following offers to me the opportunity to develop myself to become the character I wish to become.

Next month’s quests

What I intend to achieve next month are:

· Develop a better system – I am quite confident of the north start I am following now, so what I can do better is to improve on my system.

“You do not rise to the level of your goals. You fall to the level of your systems”

– James Clear, Atomic Habits

There are a lot of things presented in self-help and success books, universal principles of success which cannot be denied and has worked for the 1% who have achieved greatness. These are habits which I need to learn to adopt and integrate into my system.

· Next property purchase – I will need to begin to draft out my plan of purchasing another property by 30th June 2022. I have it written down as my goal and stuck next to my bed where I can see it every day. Things which I will need to do are:

o Create a financial forecast

o Liaise with Mrs.Shift on Perth vs. Adelaide vs. Brisbane

o Ask for a pay raise (so this will help with my borrowing power)

Mrs.Shift

Whilst we haven’t been posting much, I’ve been consistent with tracking my finances each month.

| Month | Stocks | Delta | Notes | Property | Delta | Cash | Delta | Notes |

| Jul-21 | $22,258.85 | $65,466.94 | ||||||

| Aug-21 | $23,365.76 | 4.97% | $530,000 | $25,940.71 | ($39,526.23) | For deposit | ||

| Sep-21 | $19,619.56 | -16.03% | Sold shares | $535,000 | 0.94% | $30,830.07 | $4,889.36 | |

| Oct-21 | $19,967.57 | 1.77% | $535,000 | 0.00% | $29,982.25 | ($847.82) | ||

| Nov-21 | $22,221.46 | 11.29% | $537,500.00 | 0.47% | $29,340.17 | ($642.08) | ||

| Dec-21 | $23,220.74 | 4.50% | $537,500.00 | 0.00% | $28,542.90 | ($797.27) | ||

| Jan-22 | $21,933.56 | -5.54% | $547,000.00 | 1.77% | $27,169.08 | ($1,373.82) | ||

| Feb-22 | $23,145.96 | 5.53% | $547,000.00 | 0.00% | $28,663.20 | $1,494.12 |

Monthly Summary

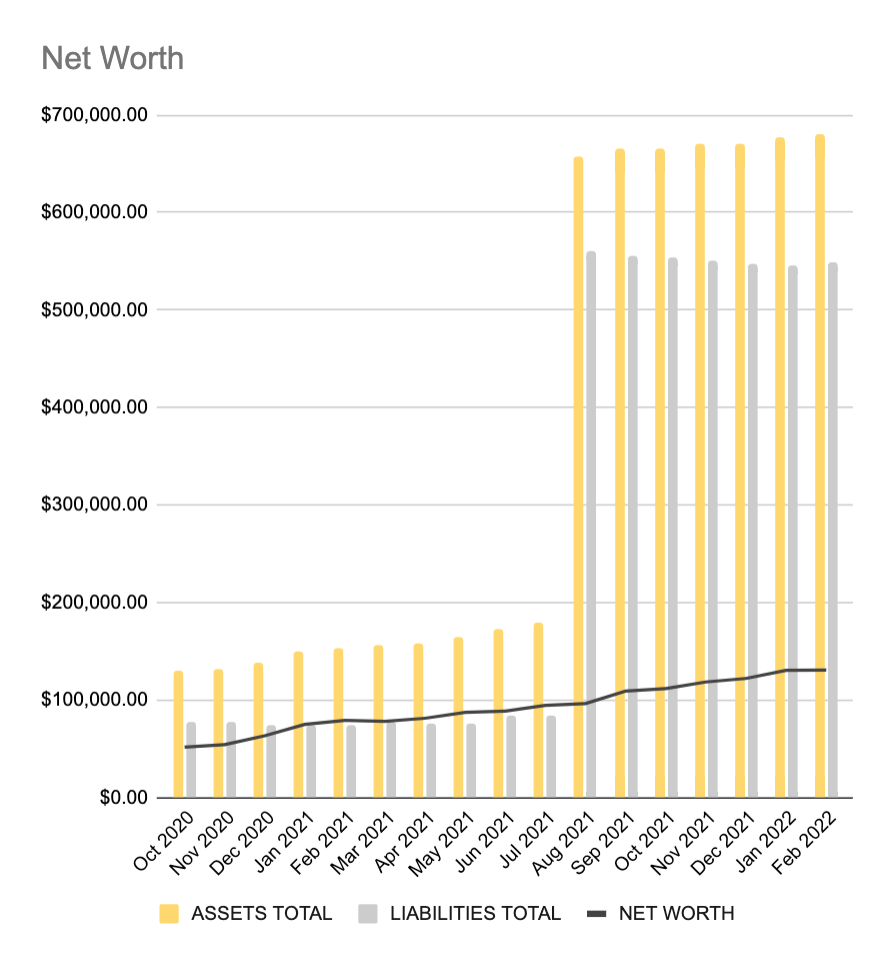

I anticipated back in October that I would steadily be spending quite a bit over the Summer. Don’t be fooled with February – I actually got a rewards credit card as well, and as such, it doesn’t tell the full story. You can kinda see my net worth plateau from Jan to Feb in the above graph.

People weren’t lying when they said that once you start ‘adulting,’ the unexpected costs just keep popping up. For example, I had to get several contractors in related to a minor shower leak; mould removal, re-grout, re-silicon.

Now, the reason I got a rewards credit card was so that I can leave money in my offset account a bit longer, maximise on saving interest, and also accumulate awards points. In particular, I chose the ANZ Platinum Frequent Flyer credit card as it had a free first year (I’ve had the tier lower than this one about 4-5 years ago) and comes with bonus points for minimum expenditure in the first 3 months. On top of that, the insurances it comes with will give me some peace of mind. In a year’s time, I plan to cancel and shop around for the next one.

Current Trajectory

I’m currently saving for the next deposit for an investment property. Whilst Mr. Shift is continuing to live at home with his parents, and has a positively geared investment property, he doesn’t have to worry about making mortgage payments like I do. On top of that, he will likely have access to property equity from capital growth much sooner than I will. So my journey to my next property will likely be much slower than his. Because of this, I have determined that I can afford to save reasonably towards a ~$60k deposit, which means I should be able to afford a property up to around $450k.

That being said, whilst saving I plan to determine where is the next place to buy. I’m looking between Brisbane, Perth and Adelaide.

Brisbane, because despite it already being on a high, the upcoming 2032 Olympics means that federal government money will be poured into the city which may further encourage capital growth.

Perth because it has proven to be quite a good market for jobs, and hence, growth. Being unrivalled by any other city on the Australian west coast, it holds a ‘monopoly’ which may continue to encourage capital growth.

Adelaide is the final option – I can’t say I know too much about it, but Mr. Shift has a good friend who was investing in Brisbane, and who has since changed his direction towards Adelaide. So I plan to look more into it.

I utilised realestate.com.au to determine wha 3-2-2 suburbs in Perth / Adelaide I may be able to afford by following these parameters:

- Sold $350k – $400k (noting that by the time it comes to buying, I prices may have shifted higher)

- 3-2-2

- Minimum 500m^2

With the list of suburbs I got, I utilised yourinvestmentpropertymag.com.au to note down the 12 month capital growth, 10 year average capital growth, and rental yield.

Next Month’s Quests

With my list of suburbs I can afford, my next step is to research the areas I found in Perth and Adelaide using PropertyChat.

If I purchase in Brisbane again, I will likely follow in Mr. Shift’s footsteps and purchase in Logan. Given my affordability, I’m happy with the idea of rental yield, current capital growth rates, and the fact that it is mostly not a region that can be extended (i.e. not a lot of new developments). This might be a future month’s quest.